Most financing programs don’t fail all at once.

They start showing smaller operational signals first.

Rising first payment defaults. Declining conversion rates. Increasing customer acquisition costs. Repayment friction. Data expenses that erode profitability over time.

Many companies treat these as isolated issues instead of recognizing them as signs of operational strain across the financing lifecycle.

The organizations that adapt fastest are usually the ones that identify these signals early, before costs compound and performance deteriorates further.

Because operational strain is rarely caused by one metric alone.

More often, it’s the result of multiple systems working against each other.

Below are some of the most common signals that something in the system may be misaligned.

1. Consumer Interest Is High — But Conversion Rates Stay Low

One of the earliest signs of operational strain is strong consumer interest paired with disappointing conversion rates.

This often happens when financing programs optimize heavily around risk reduction while unintentionally creating friction in the customer experience.

Credentialing is a good example.

Many modern underwriting tools allow lenders to access a customer’s banking transaction history with permission. From a risk perspective, this can provide valuable insight into affordability, income behavior, and spending patterns.

But operationally, it can also create friction.

Some customer segments, particularly prime or near-prime consumers, may hesitate to provide banking credentials during the financing process at all.

The result is a financing program that appears sophisticated from an underwriting standpoint but struggles operationally because otherwise qualified customers abandon the process before funding.

In this case, the issue is not necessarily underwriting quality.

It’s a mismatch between the process and what the market is willing to tolerate.

This is one of the most important realities in lending and embedded finance:

A process that looks optimal on paper can still fail operationally if it creates too much friction for the customer.

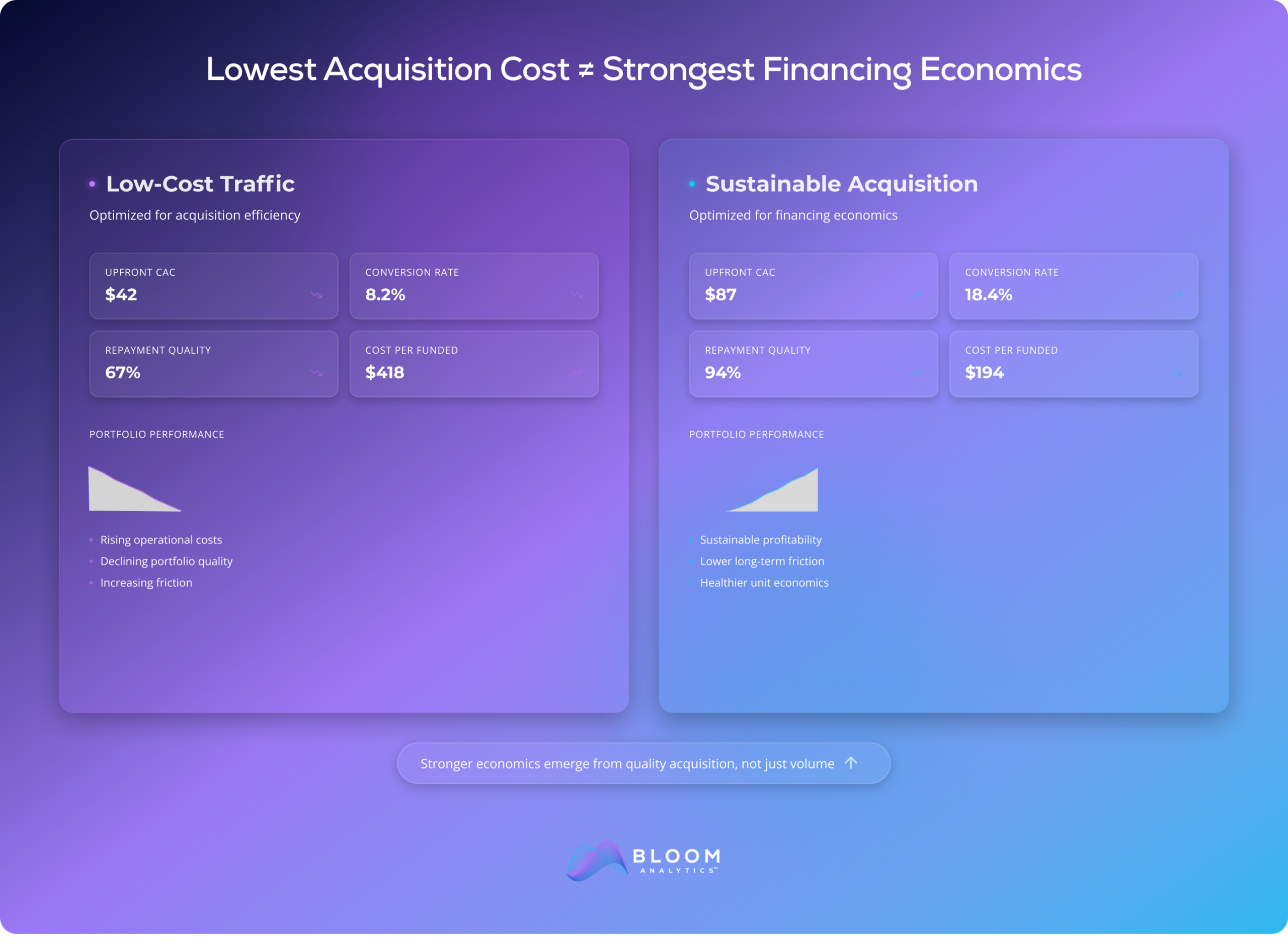

2. Customer Acquisition Costs Keep Climbing Without Better Outcomes

Operational strain also shows up in acquisition economics.

Not all acquisition channels behave the same across different financing models. Yet many organizations evaluate channels too narrowly.

For example, a company may reject a traffic source because the upfront costs appear too high and choose a cheaper alternative instead.

The low-cost traffic source, while initially appearing efficient, may ultimately generate weak conversion rates, poor repayment performance, or unsustainable funding economics.

Meanwhile, a more expensive acquisition source may actually perform better overall because repayment quality and funded conversion rates are significantly stronger.

Patterns in how different traffic sources behave eventually become recognizable through experience, iteration, or working with teams who’ve seen them before.

But the goal should never be to find the cheapest acquisition channel.

The goal is sustainable economics across the full financing lifecycle.

3. Data Costs Quietly Start Consuming the Program

Another overlooked operational strain signal is excessive data spend.

Many financing programs continue layering expensive third-party data deeper into the underwriting process without filtering out poor-fit traffic early enough.

Over time, this creates a situation where companies spend heavily evaluating applications that were unlikely to perform well from the start.

For example, some financing programs rely heavily on expensive third-party data across nearly every application that enters the funnel.

But if lower-cost scoring models or earlier-stage filters could identify clearly high-risk traffic sooner, those applications may never need to reach the more expensive stages of evaluation in the first place.

The result is not just lower data spend.

It’s a more efficient underwriting process overall.

Operationally mature lenders typically sequence their evaluation process more efficiently.

Lower-cost data sources may be used earlier to identify obvious risk indicators or eliminate clearly undesirable traffic before more expensive data sources are triggered later in the funnel.

The objective isn’t simply reducing the number of data transactions.

It’s reducing the total data cost per funded loan.

That distinction matters.

4. First Payment Defaults Begin Rising Earlier Than Expected

First Payment Default (FPD) is often one of the clearest signals that operational strain has begun affecting portfolio performance.

But rising FPD rates do not always mean the underwriting model itself is failing.

In many cases, the issue is operational.

For example, repayment timing may not align with how customers actually receive income. Debit attempts may occur before payroll deposits clear. In other words, repayment structures may not reflect real-world affordability behavior.

A borrower who could otherwise perform successfully may still default early if the payment process itself is misaligned with cash flow timing.

This becomes particularly important in embedded finance environments where companies may be entering lending without deep servicing or collections experience.

High FPD rates are often treated as purely a credit risk issue when they may actually signal broader operational friction between repayment infrastructure and customer behavior.

The key question is not simply:

“Are defaults rising?”

It’s:

“Why are they rising, and where in the process is the friction beginning?”

5. Repayment Performance Weakens After the First Payment

Operational strain doesn’t stop at the first payment.

What happens after the first successful payment often reveals whether a financing program truly understands repayment behavior.

Strong lending operations recognize that repayment performance follow specific trends.

If the first payment clears successfully, future payment performance may improve significantly. If the first payment fails, the probability of future payment failures often increases as well.

Understanding these trends can help companies diagnose where friction may be occurring beneath the surface.

For example, a company may discover that certain payment methods consistently underperform others. ACH repayment behavior may look very different from debit card repayment behavior. In other cases, repayment performance may vary across customer segments, repayment schedules, or servicing workflows.

It’s not enough to monitor defaults at a high level.

Understanding the behaviors and operational patterns contributing to them is key.

The Bigger Problem: Operational Inflexibility

Across all of these signals, one theme appears repeatedly:

Operational rigidity.

Many lending and financing programs are launched around fixed assumptions:

- A specific underwriting model

- A specific acquisition strategy

- A specific repayment structure

- A specific approval workflow

But lending environments change constantly.

Consumer behavior changes. Acquisition channels evolve. Economic conditions shift. Customer tolerance for friction changes over time.

Strong financing operations build flexibility into the system from the beginning.

Instead of treating every KPI as a fixed rule, they evaluate how different operational variables interact to produce the desired business outcome.

Is operational strain quietly affecting your financing program?

At Bloom Analytics, we help lenders and embedded finance programs evaluate repayment behavior, underwriting performance, acquisition economics, and operational inefficiencies using real-world lending data.

Schedule a strategy conversation to identify where operational friction may be affecting performance before costs and complexity continue creeping up.

Found this article Insightful? Share on LinkedIn.

DISCLAIMER: This content is for informational purposes only and does not constitute legal, compliance, or financial advice. Organizations should evaluate their specific obligations under applicable laws and regulations before implementing any strategies discussed.