When companies start exploring customer financing, the early conversation usually centers on conversion.

If customers could pay over time, would more of them buy?

Often the answer is yes. When executed responsibly, financing can unlock demand that already exists. But once a program goes live, a different set of questions starts to matter just as much:

- How do these customers actually perform once credit is extended?

- What does it cost to originate and service each financed purchase?

- Where does risk start to accumulate as volume grows?

These are the questions that shape whether financing becomes a durable growth lever or an operational headache.

And many early programs underestimate them.

Knowing Your Customer as a Buyer Is Not the Same as Knowing Them as a Borrower

Most businesses understand their customers extremely well from a retail perspective. They know which products resonate, what price points convert, and when customers are most likely to purchase. Over time, they build a strong sense of what drives repeat sales and loyalty.

Financing introduces a different lens.

A customer who looks ideal from a retail standpoint may behave very differently as a borrower.

Consider a contractor purchasing a $4,000 piece of equipment. From the retailer’s perspective, this may be a loyal customer who buys regularly and has steady income through their work. But from a financing perspective, the same customer may have a thin credit file, irregular income patterns, or limited credit history.

None of those factors matter much in a traditional retail relationship. They matter a great deal in lending.

This gap between retail understanding and credit behavior is where many early assumptions start to break down.

It’s not that the customers are “bad.”

It’s that the signals that matter for financing are often different from the signals that matter for selling products.

Conversion Lift Doesn’t Automatically Mean Profitable Growth

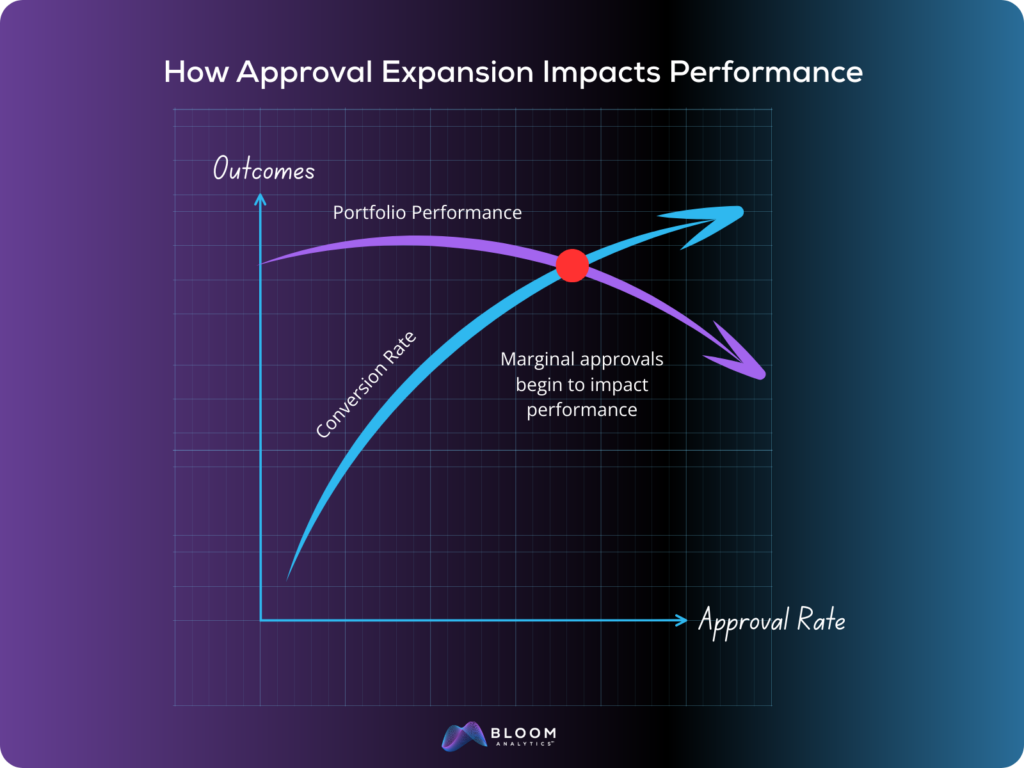

One of the biggest early surprises in financing programs is how quickly approval expansion can change the economics.

When financing is introduced, conversion rates can rise significantly. More customers qualify. More deals close. Volume grows.

At first glance, that can look like immediate success.

But approval expansion usually moves through several stages.

At first, approvals capture customers who were already likely to perform well but needed payment flexibility.

Over time, additional approvals begin reaching deeper into the pool of marginal credit risk. The program starts approving customers whose ability to repay is less predictable.

At that point, the metrics that matter most — defaults, charge-offs, servicing costs — often appear later than the initial conversion gains.

That lag can make early performance look stronger than it ultimately becomes.

Another important consideration is that approval decisions must operate within lender risk standards as well as applicable legal and regulatory requirements. Those constraints shape how approvals can expand and can also influence the underlying economics of a financing program.

Taken together, conversion lift, credit performance, operational costs, and regulatory boundaries all play a role in determining whether approval expansion ultimately supports sustainable growth.

Where Risk Quietly Creeps In

Risk rarely shows up in a single dramatic moment when financing programs launch. More often, it accumulates gradually in places teams were not initially watching.

Verification friction

Adding identity checks, income verification, or bank validation can reduce risk, but each additional step may introduce friction into the customer journey and lower conversion.

Approval expansion

Opening approvals too quickly can move a program deeper into marginal credit segments where repayment becomes harder to predict.

Operational costs

Customer support, servicing workflows, and manual underwriting reviews all tend to grow as financing volume increases.

Data costs

Third-party data pulls and bureau checks may seem minor individually, but they can escalate quickly as application volume scales.

Individually, none of these factors may seem alarming. Together, they shape the real unit economics of a financing program.

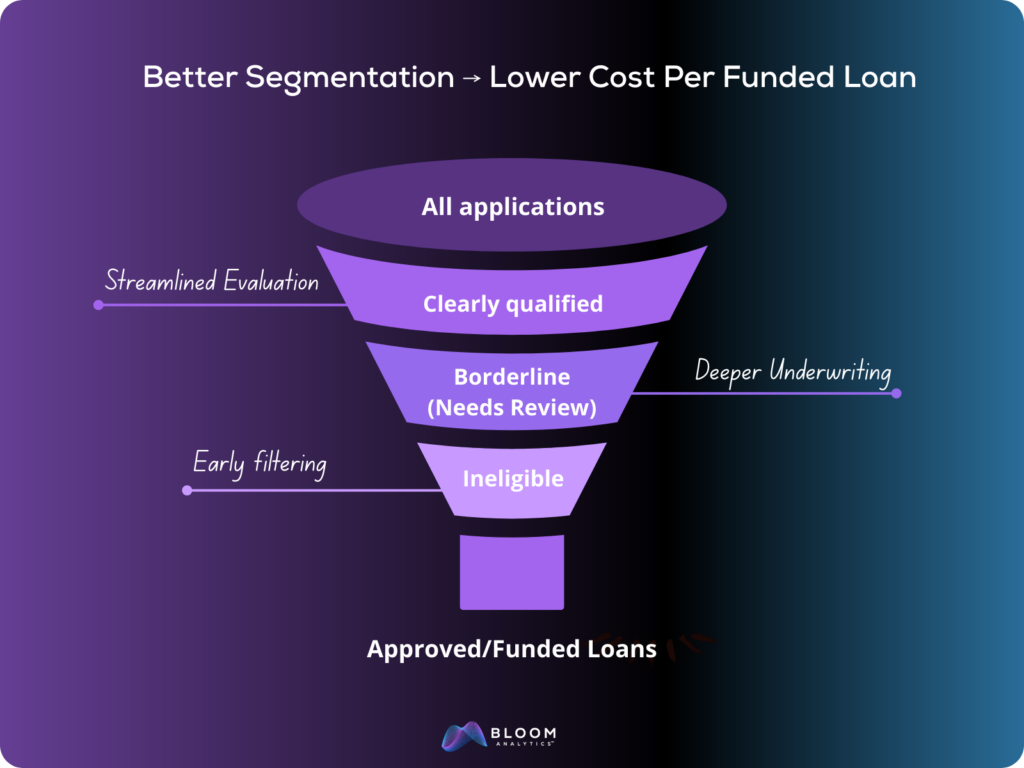

Evaluating Every Application the Same Way Can Be Expensive

Another pattern that often emerges as financing programs grow is cost inflation caused by treating every lead equally.

Not every financing application deserves the same level of evaluation.

Some applicants clearly meet risk criteria. Others clearly fall outside acceptable thresholds. A smaller group sits somewhere in between.

When every application moves through the same verification process, companies end up spending time, data costs, and underwriting effort on leads that were unlikely to convert or perform well in the first place.

More mature financing programs often evolve toward risk segmentation earlier in the funnel. The goal isn’t to lower standards but rather focus effort where it produces the most value.

Why Lenders Care About These Signals Too

These dynamics matter not only for companies exploring embedded finance, but also for lenders evaluating potential partners.

When a lender considers supporting a retail financing program, they are not just evaluating customer demand. They are evaluating whether the business understands the operational realities of lending.

Does the company understand how its customers behave as borrowers?

Is the approval strategy disciplined or overly aggressive?

Is the program structured to scale responsibly?

Programs that expand approvals too quickly or lack clear risk segmentation can burn through lending capital faster than expected and produce unstable portfolio performance.

For lenders, those signals can reveal whether a partnership is likely to remain healthy as volume grows.

Why Starting Small Often Makes Sense

Because borrower behavior and operational costs are difficult to predict perfectly, it can make sense to begin with a limited rollout.

A smaller launch allows teams to observe how customers actually perform once credit is extended. It also provides an opportunity to validate underwriting signals, understand operational costs, and refine approval strategies before scaling.

Instead of relying entirely on projections, companies gain insight from real portfolio behavior.

Those insights often shape a more stable approach to growth.

Start With a Clear View of the Economics

Financing can absolutely unlock meaningful growth. But it works best when companies understand the full picture early — not just demand, but risk, cost structure, and operational complexity.

The companies that navigate this transition most effectively tend to pressure-test their assumptions before committing significant capital or infrastructure.

A structured data study can help uncover:

- What signals in your existing data could support credit decisioning

- How quickly financing decisions could realistically be returned

- What level of risk segmentation may be achievable

- Where risk and cost are most likely to emerge as volume grows

From there, the path forward becomes much clearer.

If you are exploring customer financing and want to better understand the economic and risk dynamics specific to your business, request a free data study to pressure-test your assumptions.

Clarity early often prevents expensive surprises later.

Found this article Insightful? Share on LinkedIn.

DISCLAIMER: Insights from the data study are illustrative and do not constitute a credit decision, financing approval, or commitment.