“We sell a high-ticket product. Should we offer financing?”

It sounds like a straightforward question. But the real answer is more layered than most companies expect.

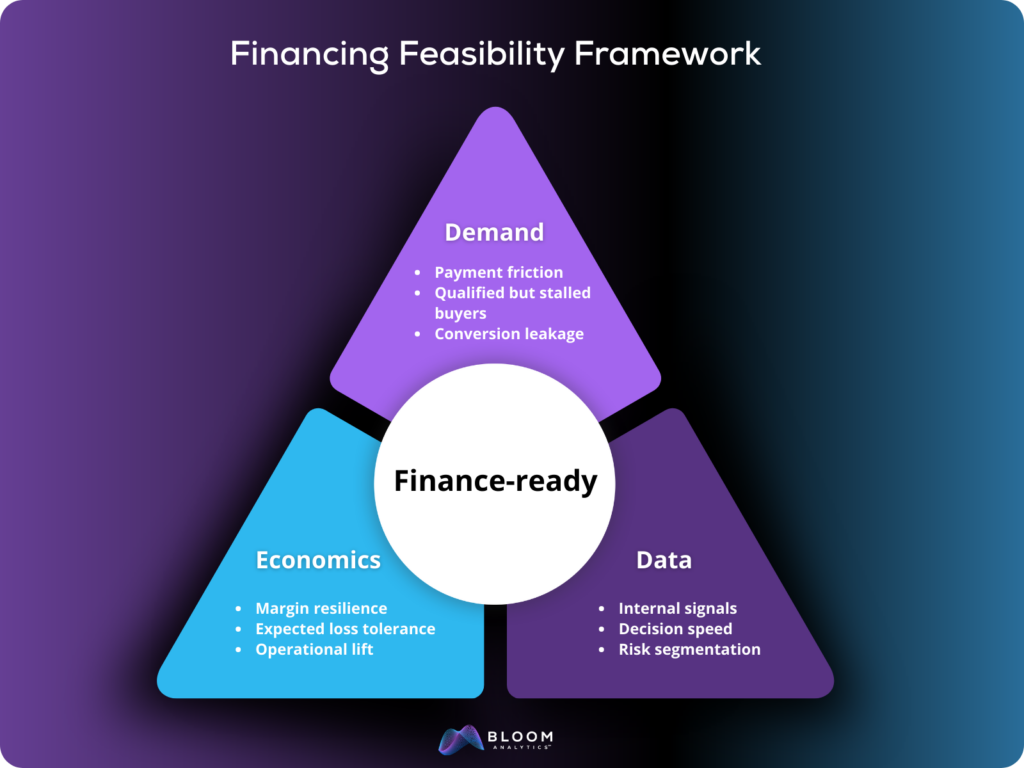

Embedded finance, and customer financing strategies more broadly, only make sense when three things align: demand, economics, and data. Miss one of those, and what looks like a growth lever can quietly become operational drag.

Let’s unpack that.

Where Are You Losing Customers?

Financing works best when it unlocks demand that already exists.

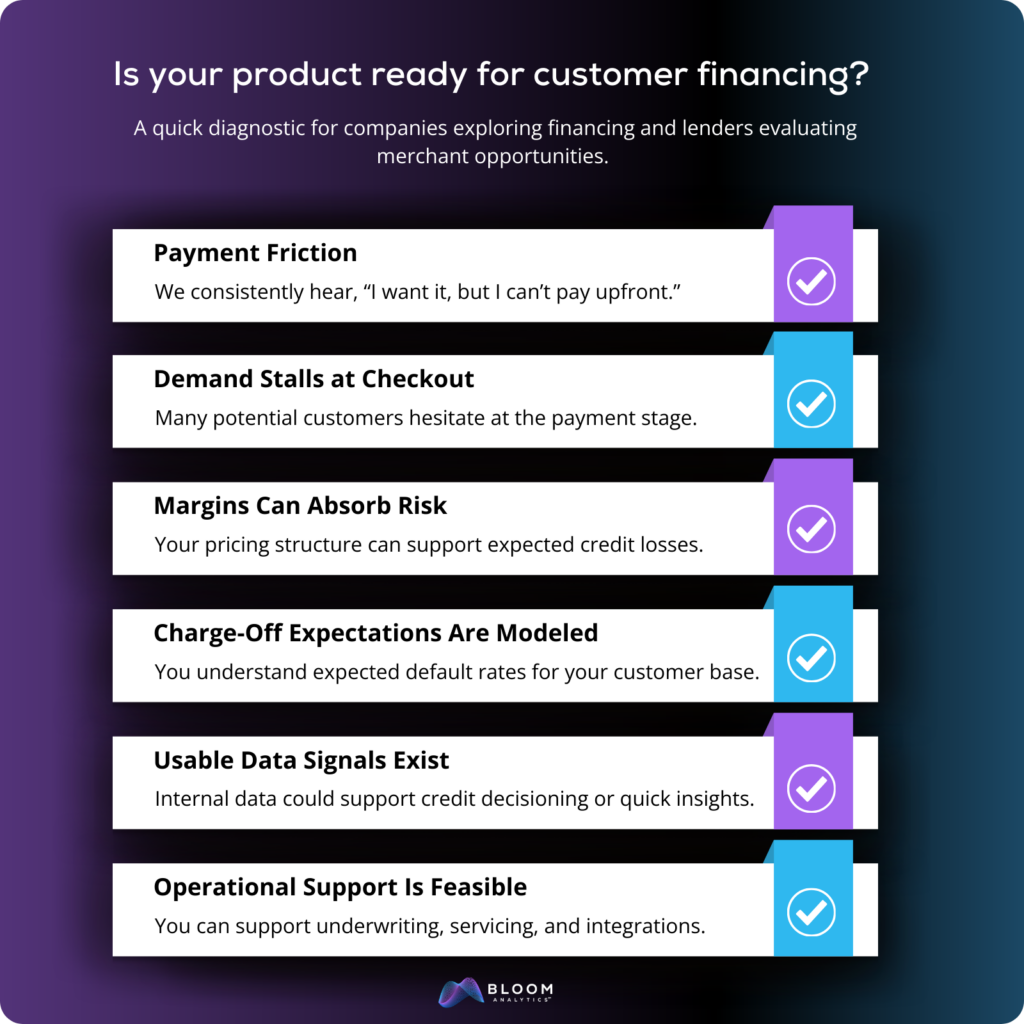

Sales teams often feel this before dashboards confirm it. They hear, “I want it, but I can’t pay all at once.” They see applications that almost qualify. They notice customers with steady income but unconventional profiles.

Thin credit files. Imperfect but improving histories. Gig workers. Under-banked consumers.

These are not automatically high-risk borrowers. They are often just underserved by traditional underwriting models.

If a meaningful portion of your potential customers want the product but stall at payment, financing may increase conversion. If that pattern is not there, layering on lending will not manufacture it.

The first question is not whether you can lend.

It is whether you are already losing willing customers because you do not.

Do the Economics Actually Work?

The product matters. Is that obvious?

Of course no one considers financing for a five-dollar add-on. But a high price tag alone does not mean finance-ready.

Financing works when customers can afford the monthly payment and the business can remain profitable after taking on the lending risk.

If a customer can comfortably handle $150 per month but not $4,000 upfront, financing removes timing friction. The intent is there. The income supports the installment. The barrier is liquidity, not ability.

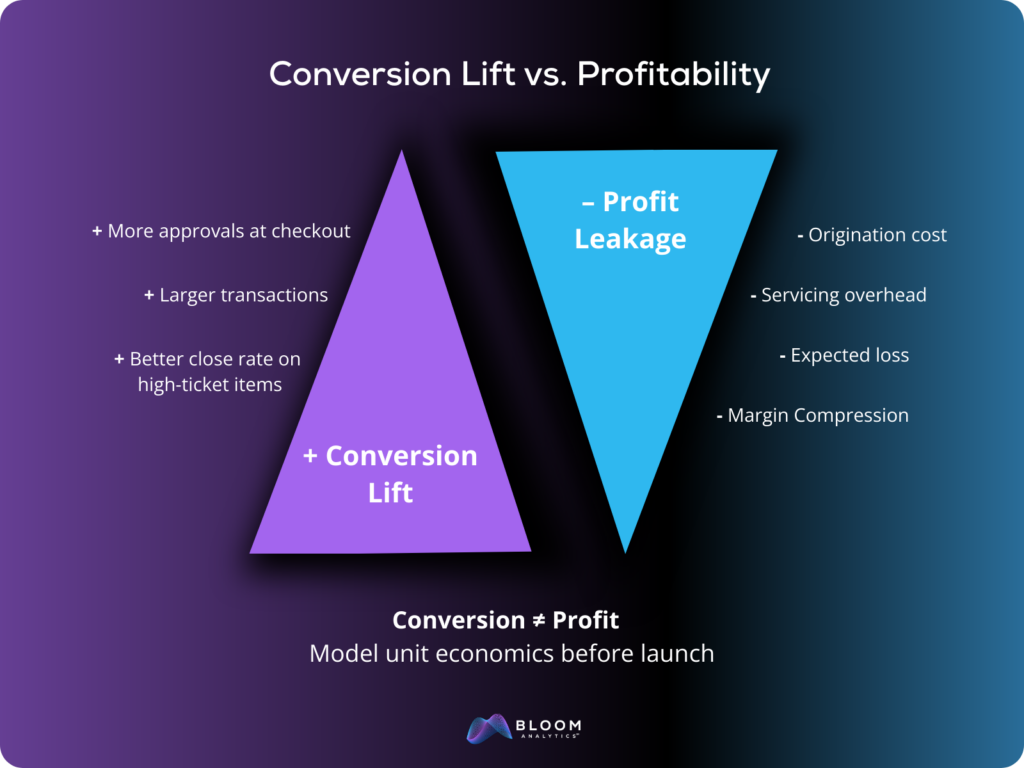

But that is only half the equation. Conversion lift alone does not guarantee profitability.

If offering financing increases conversion by 20 percent, that sounds great. But now ask:

- What does it cost to originate and support these customer accounts?

- What level of customer default or charge-off should you expect?

- What operational lift is required to support underwriting, servicing, and point-of-sale integration?

- What portion of margin are you giving up to make the financing work?

These inputs typically come from portfolio benchmarks, pilot programs, or a structured data study.

If the numbers still leave room for healthy returns, financing can be a growth lever.

If the margins are already thin, or demand is irregular, or the customer base is mostly prime and already using other credit options, financing may add complexity without meaningful lift.

That is why high ticket alone does not equal finance-ready. A product may cost several thousand dollars and still fail the profitability test.

Expensive is a starting point. Sustainable economics are the business case.

Does Your Data Support Smart, Fast Decisions?

Even when demand and economics align, the real determining factor is data.

A structured data study can reveal what is actually possible with your existing data. Not hypothetical models or generic assumptions. Insight grounded in your own data.

In a structured data study, we evaluate:

- What internal signals can be leveraged for credit decisioning

- Whether no-third-party quick insights are viable

- How fast decisions can realistically be returned

- What level of risk segmentation is achievable

In many cases, quick credit insights can be delivered in milliseconds. Full automated underwriting for small dollar unsecured loans can be completed in seconds. If collateral or insurance verification is required, the process may take longer, but still significantly faster than traditional lending workflows.

The goal is not just speed. It is precision. Custom, automated underwriting tailored to your product, your customers, and your risk tolerance.

Even when the strategic case is strong, the next concern is usually operational complexity.

You Don’t Have to Build It Alone

Offering financing doesn’t mean becoming a lender overnight.

In many cases, the smarter path is structural alignment. That may mean connecting with an experienced analytics partner. It may mean building custom, automated underwriting tailored to your specific lending needs. It may mean integrating regulatory and compliance expertise from the beginning rather than retrofitting it later.

The structure should fit the business model, not the other way around.

Embedded finance is not just a product feature. It is a strategic decision that touches risk, operations, compliance, and customer experience.

You do not need to solve all of that internally to explore whether it makes sense.

Start With Clarity

If you are exploring embedded finance, the smartest first step is not launching a financing program.

It is understanding whether your demand, economics, and data actually support one.

The safest first step is a structured feasibility study.

You provide relevant data. We analyze what can be leveraged. You get a clear view of feasibility, speed, and potential performance.

Then you decide.

If you are curious whether financing could drive meaningful growth for your business, request a free data study and see what is realistically possible.

Clarity first. Infrastructure second.

Found this Insightful? Share on LinkedIn.

DISCLAIMER: This content is informational only and does not constitute legal, regulatory, or compliance advice. You remain fully responsible for fair lending compliance, FCRA requirements, and all applicable lending laws. A feasibility study provides data insights only; separate legal and compliance review is required before implementing any lending program.